An excerpt from Your Multimillion-Dollar Exit: The Entrepreneur’s Business Success(ion) Planner.

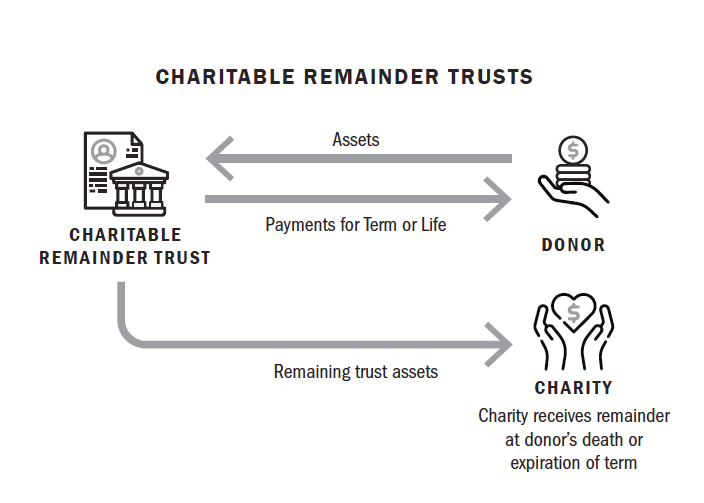

Of the various charitable planning techniques that people use either before or after an exit, one of the most popular techniques - particularly as interest rates rise - is known as the charitable remainder trust (CRT). In a CRT, you’re giving a portion of your business interest to a trust that ultimately, at the end of the term or your life expectancy, will be paid out to the charity.

- Income Tax Consequences – A CRT generally is funded with appreciated property, e.g., stock in your business.

- You should not use S corporation stock, because a CRT is not an eligible shareholder of an S corporation.

- You should avoid a partnership or LLC interest treated as a partnership, if the interest will generate unrelated business taxable income and destroy the tax exemption of the trust.

- If appreciated stock is used to fund the trust, you will be entitled to claim an income tax deduction for the gift of the stock to the CRT in an amount equal to the fair market value of the charity’s remainder interest.

- The charitable income tax deduction is limited to 20% of your adjusted gross income for the year of the contribution for gifts made to a CRT, the beneficiary of which is a private foundation (a/k/a charitable family foundation) or 30% for gifts involving public charities.

- Any amount not deductible due to the limitation can be carried forward and used in the next five tax years. One important requirement is that the value of the charitable remainder interest must be more than 10% of the total value of the trust.

Importantly, as long as the interest being transferred is not subject to debt, you can avoid income tax on the transfer of the appreciated business interest to the trust and on the sale by the trust of the interest.

Moreover, the CRT will not be taxed on any income it generates (provided that the trust invests only in investment assets, such as stocks, bonds and other income-producing or capital-appreciating assets).

Note: You should avoid reinvesting the proceeds from the sale of the property initially contributed to the trust in tax-exempt securities. If you do so, the IRS may try to tax the sale directly to you, ignoring the existence of the trust. Also, you must not invest the proceeds in other businesses that generate unrelated business taxable income to the trust – this will destroy the CRT’s tax-exempt status.

The CRT generally will be required to pay you a percentage of the value of the trust assets (i.e., at least 5% per year) annually. The type of trust (unitrust or annuity trust) will determine how much income must be distributed annually. The amount distributed generally will be taxable to you to the extent it is paid out of the trust’s current and prior years’ ordinary and capital gains income. Any amounts paid to you out of principal (other than capital gains that are considered part of principal) generally will not be taxable to you.